Can't find what you are looking for? Call our customer support at 1300 856 710 or email us at info@austbook.net

Do you want to become a registered BAS Agent but you're not sure where to start? We've provided an outline of the qualifications and registrations required for this profession.

Wondering how to become a registered bookkeeper? Here's an outline of what to expect when working as one and the steps required to become certified and start your own bookkeeping business.

Explore the requirements for gaining relevant experience

Experience benefits like nowhere else with ABN. Explore all the products and services which make up your membership.

Explore all the products and services which makes up your ABN membership.

Meet the team at Australian Bookkeepers Network.

Find out how a bookkeeper can help your business.

Protect your Bookkeeping Business with ABN's PI Partners.

Protect your business with Cyber Insurance

How ABN gives back to the community

ABN is committed to providing professional development opportunities for bookkeepers.

Members Can Access Australian Bookkeepers Network's Bookkeeping Checklists, Contract Samples, Quote Templates, Agreement Letters & More. Join Today!

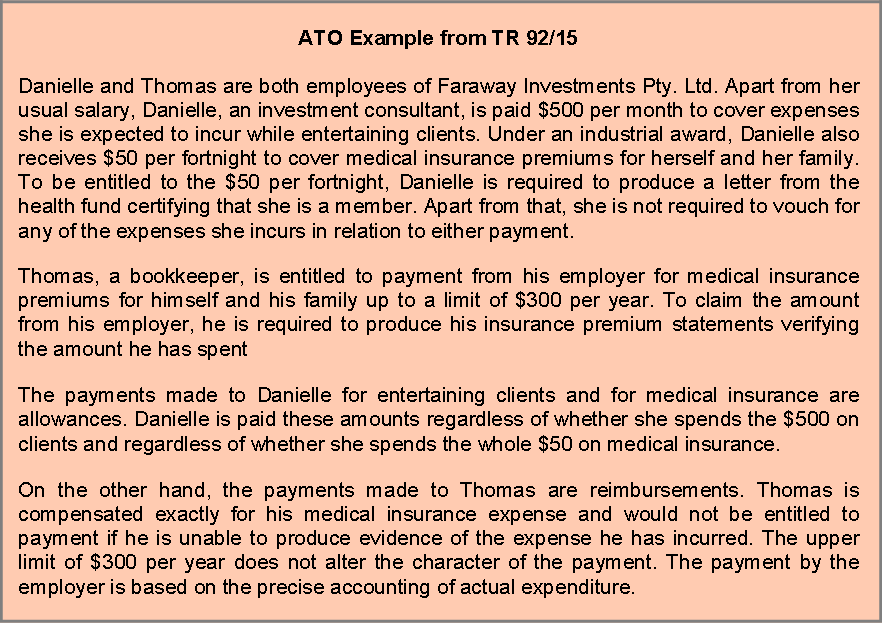

For the many bookkeepers who handle payroll, according to the ATO the treatment of allowances is one of the most misunderstood areas. Whether it be misclassifying an amount as an allowance (when it's actually a reimbursement) or applying the incorrec

From the outset it’s important to define an allowance, and in particular distinguish it from a reimbursement as the payment summary, PAYG withholding, superannuation and payroll tax treatment can differ significantly. On the one hand, allowances:

Conversely, reimbursements:

An allowance is a definite sum of money allotted or granted to meet expenses or requirements. An allowance usually consists of the payment of a definite or pre-determined amount to cover an estimated expense, and is paid regardless of whether the recipient incurs the anticipated expense. An amount is not an allowance if it’s just folded in to normal salary and wages. Rather an allowance must be a separately identifiable payment made to an employee.

Conversely, a payment is a reimbursement when the employee is compensated exactly (i.e. precisely, not approximately), for an expense they have already incurred. The employer considers the expense to be their own, with the employee effectively incurring the expenditure on behalf of the employer.

Having determined that the amount is an allowance, the PAYG rules require that certain types of allowances are subject to withholding whilst others are not, while the payment summary treatment can also differ markedly depending on the nature of the allowance paid. By using these Tax Office tables you can eliminate PAYG withholding and payment summary reporting errors going forward.

Regarding superannuation, the general rule is that all allowances received by an employee, except for expense allowances that are expected to be fully expended and allowances that are fringe benefits (e.g. LAFHAs), will attract superannuation. However, where an allowance relates to work outside ordinary hours, it will not attract superannuation (for example, overtime meal allowances).

Article written by Australian Bookkeepers Network (ABN)

To find out more about ABN visit www.austbook.net